Eco Animal Health (ECO) - A recovery play and a blue sky play

Cloudy situations can sometimes be the best investments

Eco Animal Health, on the surface, is a company that does one thing well: their Aivlosin antibiotic drug for pigs and poultry. They are relatively successful here, having a strong global market share. Their main line of business is profitable, and should be stable, except for two factors which I’d go into below, that have impacted revenues and profitability in the past 2-3 years.

However, they are also pursuing a strategy of diversification, into vaccines. They have spun up an R&D arm, focused on getting vaccines from idea to approval. They have heavily invested in this area, and 2024 will be critical. More details below too.

So this share is very tricky to value, as the core business now should be valued as a recovery play, but there is an imminently emerging pharma blue-sky growth business attached. However, judging from the share price action, investors aren’t really buying into this. Which is expected, because blue-sky investors are different from mature pharma investors.

So is there an opportunity now to invest?

The Recovery Play for the core business

Their core product, Aivlosin, is highly profitable and they command a good market share globally. This is the cash cow for Eco Animal Health, but generic competition have been slowly chipping away in their markets. However, I do not see this as a major threat, as some sort of market equilibrium has been reached.

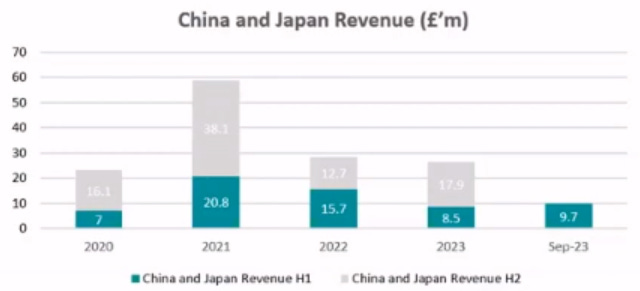

Over the last 2-3 years, they have been hit hard by two major factors. One is the global spread of the PRRS virus in pigs, which have massively disrupted pig farming. This in turn has caused volatility for Aivlosin demand; when pig herds are reduced, less pigs means less demand for Aivlosin, obviously. The second factor is the boom and bust cycle in China; pork prices in China have massively fluctuated over the past 2-3 years. Pig farmer finances have been stretched, and Aivlosin usage is curtailed when pork prices are low, and farmers can’t afford it. Right now, prices are low, maybe even below break-even for most pig farmers.

China used to be like 30-40% of total Aivlosin revenues, so this has had a major impact on revenues. You can see from the chart below (Japan is very small compared to China revenues in all years):

I am expecting a normalised full-year revenue run rate of like £40-50m from China, compared to perhaps £22-27m expected for FY24.

I don’t expect an improvement in either the PRRS situation or the China situation before Q4-24. There is a potential PRRS solution, but this will only hit the market in late 2024, at the earliest. The China weak price situation will depend on herd reductions as well as increased consumer demand, both of which unlikely before Q4-CY24 too.

Still, the business is somewhat profitable. In HY-Sep23, I estimate normalised PBT of £0.8m, excluding the R&D investments, from the core Aivlosin business. Not great on £38m of revenues, but at least surviving and profitable.

The blue-sky growth play with the vaccines

The cloudy investment case here is all down to the blue-sky R&D strategy. They have sunk in a lot of money over the years, with numerous delays, to try to commercialise new vaccines.

They need to get approvals this year, and the earliest commercial revenues is only expected to start in 2025. In the half year to Sep23, they spent £3.6m on R&D, on existing revenues of £38m and adj EBITDA of £0.7m. So a fairly heavy bet! For 2024 and first half of 2025, they are expecting another c£10m of R&D needed for the final hurdles to get the first two vaccines into market.

They can afford to invest. The main Aivlosin business is cashflow positive, and they have £9m net cash on hand as of Sep23, as well as £15m of undrawn banking facilities.

How then, to value this? They have sunk in £42m into R&D since Mar20 (not sure if there was investment before this) until Sep23. And no revenues yet to show for it! Granted, some of it might be R&D into Aivlosin and not just the vaccines, but even taking three quarters that amount of £31.5m, is a lot of R&D. The market cap is £60m at the moment.

How to value

The value play recovery is probably the easiest one. And there are several ways to get to a figure.

One could take the 2021 EPS of 10.9p, when there was a “boom” in China revenues. This seems plausible, as they managed to get the same or more in FY19 (10.9p) and FY18 (14.1p). Since then, non-China revenues have grown too. Even taking a conservative 80% of this, gives an EPS of 8.7p. The current share price (86.5) is barely pricing in a 10x PE.

The other way is bottoms up from FY24 forecasts. Currently, the EPS forecast for FY24 is 2.0p. If you reverse out the R&D spending being charged to the P&L, you can probably add another +4.4p to this, so the currently EPS is c6.4p. If a recovery in China adds in another £10m revenues, I think this could result in another +3.4p EPS dropping to the bottom line. So that would be a 9.8p EPS, and so current share price is indicating a 8.8x PE.

As a pharmaceutical company with a proven product, good market share, and good profitability… the Aivlosin business on its own should be trading at 12x+ PE, in normal situations.

Both of these calculations, completely ignore the value of the emerging vaccines R&D. A slide from the HY Results Webinar indicates that Year 1 Revenues of the two products launching in 2025, could be worth £26m of revenues a year. Probably at high gross margins. That would be transformative to the PBT.

But how to value? That is the question. If this was a pure blue-sky pharma company, would this be valued at say 2-3x revenue of those two first products? That would imply a share price of 115p compared to 86p currently. I’d love to hear thoughts on valuation techniques of blue sky pharma, one year out of potential commercial revenues.

Conclusion

Even with these back of the envelope calculations, you can see there might be potentially bags of value at 86p. Even if the vaccines portfolio is worth nothing, the main business is still trading at a fairly cheap PE. And if the vaccines portfolio comes good, then you’re getting the core Aivlosin business for free.

The recent share price plunge (108p to 86p) has been due to investor expectations that FY Mar24 forecasts will be missed, due to the China recovery (expected in Jan-Mar) not materialising, when you look at China pork prices. Genus, another company in the same sector (but different products/services) issued a profit warning recently on weakness in China. This may prove to the buying opportunity to pick some Eco Animal Health (ECO) shares at bargain prices.

I've digested the latest TU at the end of Apr24.

Am quite bullish. I had a fear that the FY Mar24 EPS might be missed, but it is now confirmed as coming in-line.

There was a big omission of any forward looking statements... which is worrying? H2 CCY growth was probably around +5% YoY, which is much lower than the +15% in H1.

However, I think the pork situation China is getting brighter, with firm forward pricing for lean hogs already starting to come through, so this should start crystallising in the SP in the next few months.

Crunching the numbers, I think a very conservative fair price estimate is 140p, and this is assigning zero value to the vaccines, only on the As-Is Aivlosin business. Hard to give a value to the vaccines as I state in my article above, but I can imagine that once the vaccines are more tangible, a 75-100p valuation add-on is sensible. So overall, thinking a 215p to 240p share price is achievable by mid/end 2025, which is only 18 months away, and a doubling of the current SP.

Didn't realise a TU was coming out today!

The Eco Animal Health (EAH) share price had plunged recently due to fears about further deterioration in China trading. Genus had released some bearish news recently that caused that. Also, pork prices had plunged in China in early Q1.

However, the latest TU suggests that trading was resilient, despite that headwind in China. Also, pork prices have had a strong recovery over March, so that headwind is much receded now.

I've decided to buy a position this morning, taking advantage of the depressed share price. I think they have two potential huge EPS growth drivers in the next 2 years: China recovery, as well as new vaccines. All it takes is just one of those two to come true, to power a re-rating in the share price here.